Pancentric orchestrates modernised new look for Insurtech UK

New brand and website launched for trade association Insurtech UK, developed by Pancentric Digital and design partner Kohde

Insurance is more innovative than many think - and it's had a profound, empowering impact on our progress as a society. Here's a rundown of some the biggest hits of the last 50 years. Are these the most notable?

Rewind. 1666. The Great Fire of London. A third of London destroyed, 100,000 people made homeless, 50 years to put everything back together.

Necessity, as they say, is the mother of invention and modern insurance was born.

A flurry of first-movers set up. Without a single post-it note, Sharpie or whiteboard they created a mechanism for financial cover and a city-wide fire service to boot. It was a solution that focussed on prevention, not just financial rescue. Value-add thinking we'd call it today. The concept restored confidence, unlocked recovery and the rest is history.

And that’s the way it's always been. From maritime insurance in the early days through to more recent product innovations (life, term, accident, health, business interruption, cyber) - insurance has been a cornerstone to human development and trade. Check out Deloitte University Press who do a great job cataloguing insurance innovations of the past.

Fast forward to the late 20th century & beyond, insurance continues to be an innovating force for good (in the main) and moves with the times.

It’s fair to say insurance aggregators have ripped up the customer acquisition rulebook. In general insurance at least.

Within a decade of muscling into motor and home insurance, the landscape was redefined; a sobering reminder when considering emerging trends now. First came MoneySuperMarket in 1993. GoCompare, Confused, CompareTheMarket followed in the 2000s.

By 2009, aggregator purchases accounted for more than half of all private car insurance sales in the UK, and 36% of home insurance sales. According to McKinsey, ‘now almost 50% of online insurance in Europe is sold via aggregators’.

Let’s face it, the big insurers never excelled at customer sales and servicing. They didn't need to. Many are better now, but historically it's not been a strong area.

And while a good broker could do personal service brilliantly there was a vision and scaling issue - lots of independents - and tech generally wasn’t brokers' thing.

With hindsight, there was a yawning gap in the market and aggregators marched in.

Has the impact been positive? For consumers, it's been empowering and has made insurers try harder - much harder. More consumer choice, keener pricing, simpler, easier purchase. Some (insurance insiders mainly) say pricing pressures have compromised product quality with providers having to play the system and consumers less well-covered as a result.

Will it last? The model demands relentless brand investment and marketing expenditure. And cross-selling is key to the commercials. Some commentators say we're at saturation point in the UK while other territories can expect growth. There are threats. The rise of the platform players e.g. Amazon. More to come here. Changing consumer behaviours (less car ownership, more pay-as-you-go). And other factors might make life awkward - regulation changes, damaging new search algorithms to compromise web traffic.

The aggregators have had a good run and, while price remains king, may continue to dominate for the foreseeable.

Either way, aggregators' legacy has been to bring insurance kicking and screaming into the consumer age. They've also set a new standard for digital experience inspiring the next generation of wannabee change agents (aka insurtech).

Telematics - or télématique - is a made-up word, dreamt up by a couple of French chaps as part of a Government report on the computerisation of society back in 1978.

Nowadays, the term mainly refers to vehicle telematics. Bundled with insurance it's done many good things, perhaps yet to realise its full potential.

The top good thing it's done is to save lives.

Young people and cars don't mix well and many road users have died or suffered terrible injuries as a result. I know a couple who lost a teenage son in a car accident last year. It has to be one of life's all-time awful things.

The wider stats are shocking.

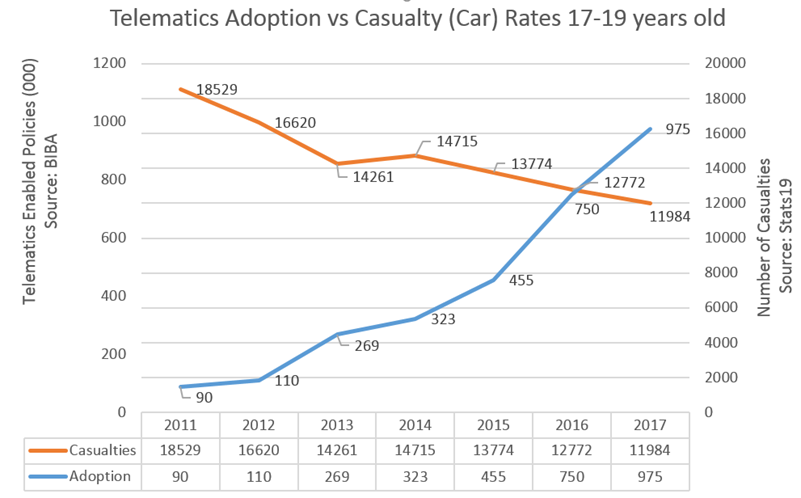

Drivers under 25 cause 85% of all ‘serious injury’ road accidents. 17-19 year olds cause 9% of all road fatalities but represent only 1.5% of drivers. Happily, telematics was invented and gained commercial traction around a decade ago.

By 2017, stats from LexisNexis Risk Solutions show that telematics had successfully reduced road deaths and serious injury among 17-19-year-olds by 35%.

The innovation and its impact (charted below) is a reason for celebration.

Chart showing the positive impact of telematics on road casulty rates for 17-19 yar olds, 2011-2017

And of course, telematics has also made motor insurance more affordable for young people. Prove you're a safe driver and we'll lower your insurance premium. Without a 'black box' most young people simply couldn't afford to take to the road.

Telematics has also helped oil the wheels of business.

Commercial fleet owners that have installed black boxes have reported a 43% reduction in collisions and a 58% reduction in speeding and fines. Same again for accidents.

1 in 10 reported insurance premiums decreasing as a direct result of telematics.

Back in 2013, there were 5.5 million telematics policies globally. Estimates suggest this will be 100 million by the end of 2020 generating in excess of €50 billion in premiums.

It's still work in progress. With 5 people still killed every day on UK roads, there is much still to do. And perhaps a few decades from now - with computers taking over the wheel - telematics in its current form will seem quaint - irrelevant even.

Either way, telematics 1.0 has made a huge contribution - and has been a life-saver for many.

After years of resisting, I recently got myself a smartwatch and knuckled down to tracking my exercise activities and sharing with friends on Strava.

I haven't gone the whole hog and wired this into a health or life insurance policy but millions of people globally have - with Discovery, better known as Vitality in the UK.

Discovery has rewritten the rules of health insurance with their shared value model.

Clearly, their proposition resonates with many.

Earn points for healthy behaviour and 'spend them' across our extensive lifestyle & financial partner network.

Says EY in their Future of Health Insurance paper, "[the model] transforms insurance from a short-term contractual relationship to a longer-term collaborative one by laying the foundation for ongoing engagement with customers".

The Holy Grail of personal data is at the heart of the transformation, step-changing how risk is assessed and underwritten. And this data is only going to get more reliable and available as devices improve and proliferate. Headaches and opportunities for incumbents.

Tellingly, Vitality refers to themselves as a behavioural platform first and an insurance company second. And it's not 'emperor's new clothes'. Analysis of their platform data reveals that activity tracking has reduced health risks by 22% and for those most engaged achieved a 10% reduction in hospital admission rates and a 14% lower cost per patient.

Discovery's success also highlights a further new trend around ecosystems and platforms, explored by McKinsey. Discovery achieved 31% annual growth in international markets by using their platform to partner securing "AIA across Asia, Generali across continental Europe, Manulife in Canada, Ping An in China, and Sumitomo in Japan".

Of the innovations covered in this article, it feels like this one most sets the tone of things to come. Data, platforms and ecosystems are fast becoming the buzzwords of now.

Discovery continues to be ambitious with a prevailing mission to make 100 million people 20% more active by 2025.

Yes, the model raises concerns around data privacy but with ongoing work on legal protections and the huge upside in improved mental and physical wellbeing (not to mention lifestyle incentives), this approach is surely destined to become the norm.

Wider government concerns around obesity might also jolly things along.

In Western societies, the tech revolution was spent sitting at desks wearing ties (rollnecks if you were lucky), and our approach to process and systems was forged from this.

Connectivity and mobile came very much second.

Now we spend eye-watering amounts of money - not always successfully - patching or replacing old computer systems to adapt to the expectations of a new digital world. And little by little we wean ourselves off the analogue habits of printing and posting things.

For territories like India and Africa the revolution has been different. For most in these regions, there's been no desktop - it's been mobile-first, mobile-only.

In the last decade, India has moved from a nation of 5m mobile phone users to around 500m; and these are smartphones. Today World Economic Forum talk about an "unprecedented pace and scale of digital adoption...driven by a near-perfect confluence of supply factors (falling bandwidth prices, low mobile device prices, rapid rollout of 4G, aggressive nativization of mobile technology) and demand factors (rapidly rising affluence, fast mobile technology adoption across demography...etc."

It's fascinating to see how insurance has developed in this environment.

In many respects, some of these high-growth regions have stolen a march on the West with examples of full life-cycle insurance management delivered entirely via mobile.

The liberalisation of the insurance industry by the Indian government in 1999 was a trigger for significant growth...and for insurance innovation.

The big innovation came around 2010, led by L&T General Insurance Company - now known as HDFC General Insurance Limited I believe.

According to the then CEO Joydeep Roy, "The idea at its core was becoming and remaining a company that depends on mobile solutions right from day one".

This was his vision 10 years ago. The sort of thing that excites insurtechs now.

The mobile-first technologies L&T invested in gave them access to a vast and disparate Indian customer base and delivered quick transactions and efficient servicing right through to claims. At the time of Deloitte's research (in 2013) "more than 100,000 policies worth $28 million had been successfully issued and more than 6,000 claims serviced, all without a single piece of paper." Impressive stuff.

In Africa, others have done similarly impressive things step-changing access to insurance using the combination of mobile, lower operational costs, and affordable micropayments.

A great example reported by the Guardian back in 2012; "A $3 monthly life insurance premium gave kettle maker Rebecca Darko and her family, from Accra, Ghana, a safety net of $140 in life insurance after a family death threatened to drown them in debt.”

While many of us in the UK privately grumble about insurance premiums, in less privileged settings the intervention of insurance can be truly liberating and life-changing.

No doubt. Insurance has had a great record of building confidence and unlocking investment, "providing a level of certainty that makes taking risk possible"(Deloitte). Just as it did in London back in 1666 when modern insurance was born.

In the case of Africa and further examples in rural China, "insurance adds value to the lives of those who most need it by doing what insurance at its very best can do; allow people to participate in economic activity that may help them up the economic ladder." (Deloitte)

New brand and website launched for trade association Insurtech UK, developed by Pancentric Digital and design partner Kohde

HUB Intranet has partnered with QBS, the largest channel-only online marketplace. QBS is the go-to software delivery platform for enterprises, providing a complete solution for long tail software procurement.

Building on recent award success and stand-out work in the specialty insurance space, Pancentric's Go-Insur policy admin solution has launched a brand building campaign in the City of London.